In Search of Hope: AS Roma’s Grim Financial Reality

By Umberto Pelà (17.12.2023)

“Not that I’m jealous, but Man City paid €80 million for Kalvin Phillips and now Pep has said it would be better for him to leave. So he’ll leave and they’ll get someone else. Our reality is very different. It’s not easy for us to sign one player.” AS Roma’s manager Josè Mourinho’s words from just three days ago thundered across Italian mainstream media, leaving fans questioning whether the Portuguese manager’s words hide the truth or a simple, classic bluff.

Curious, I chose to investigate for myself. Whilst AS Roma is no longer a public company listed on a Stock Market following its delisting in September of 2022, I dug the internet in search of the most recent financial statements, and found the composition of financial statements from the 2021-2022 fiscal year. Whilst the 2021-2022 season and fiscal year might still carry some form of negative residue from the effects of the COVID-19 pandemic, the underlying assumption for this analysis is that the financial stance of the club will not have changed exponentially in solely a year. On top of this, looking at the root of problems which arise now is rather interesting to me.

Before diving into the club’s finances we should immediately state what factors we are looking for. Above all, a soccer club’s financial health is largely defined by the balance between costs and revenues. For a soccer club, costs are built up mainly by amortization, wages, and other operating costs (such as agent commissions and bills to keep the training facilities running). On the other hand, revenues are mainly built up from ticket sales, sponsorships, and player trading. On top of that, to grant a view with a wider perspective, we should also consider the value of the club’s assets and any debt it carries — this will give greater insight to the value of the club as a whole.

In AS Roma’s case, all of the aforementioned factors do not convey a promising picture. Whilst the club’s Football General Manager, Tiago Pinto, continuously reassures the fans that the club is in a financially stable situation, its income statement does not provide support to his claims. Firstly, as mentioned in the endnotes (p54) of AS Roma’s financial statement, the club is currently battling with Financial Fair Play (FFP) rules. Whilst it has respected all its debts to other clubs, it has been under investigation by the Club Financial Control Body (CFCB) of UEFA. In other words, it has had to provide more financial information culminating in a “Settlement Agreement” — a term that has plagued Italian clubs over the past few years due to their lackluster financial situations. The Settlement Agreement provides a series of sanctions in the case that the club does not respect financial parameters set by UEFA before the 2025/2026 season. As part of the first sanction, which has already taken place, UEFA is withholding €5M from any reward pool from European competitions that AS Roma might have earned. The club has also stated that the maximum penalty is of €30M, and that whilst it suggests it has time to respect the financial parameters to avoid this penalty, it has already poured 25% of that quote (€7.5M) following financial estimations for the years to come. These total costs of €12.5M are included in the cost sections of the income statement. Not an encouraging start.

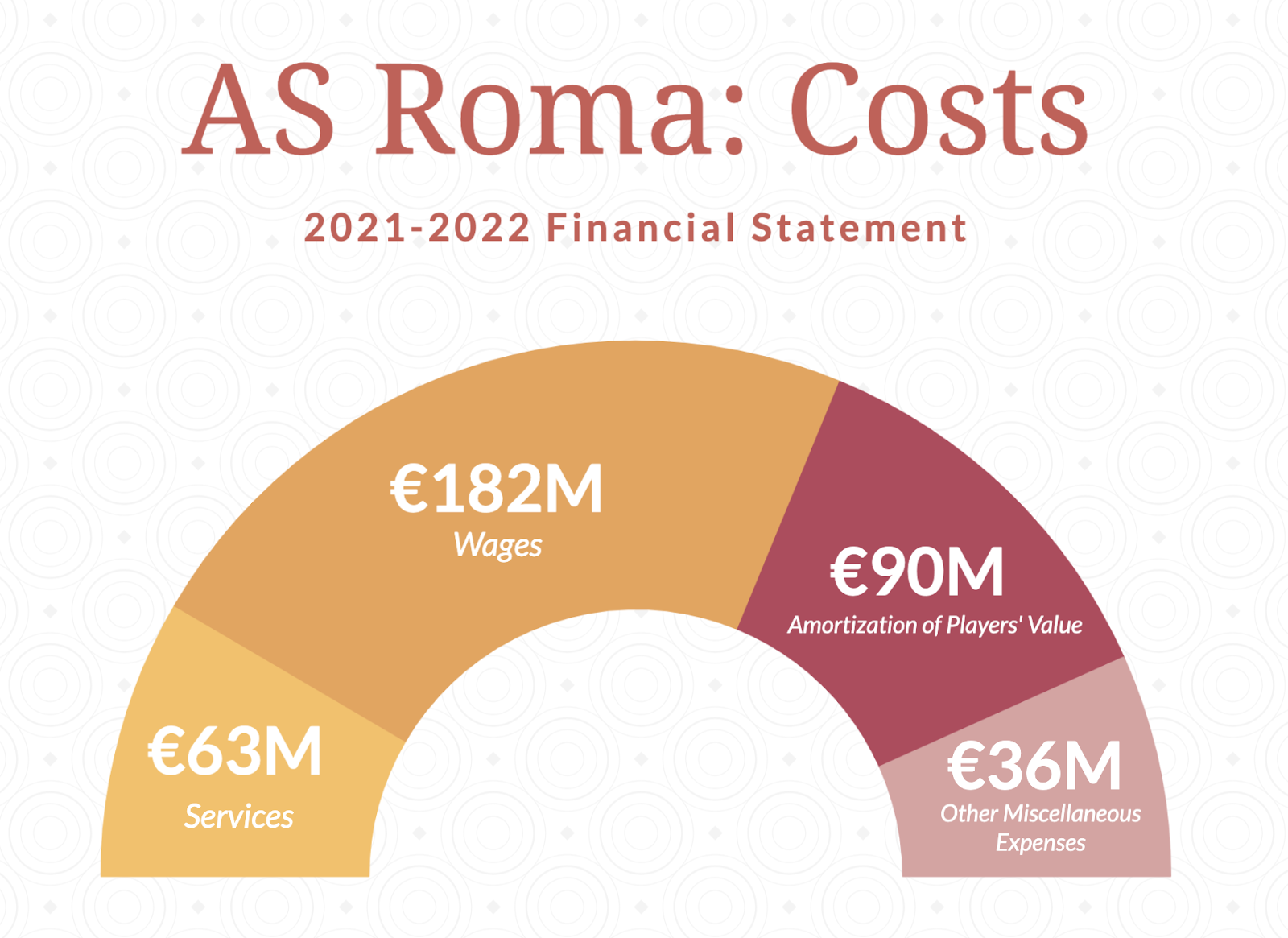

If we then shift our focus to the more current aspect of the business, we can see that above all, AS Roma has issues with its balance between revenues and costs. During the 2021-2022 season, the club incurred costs of around €400M, mainly coming from employee wages (Coaches, Players, Staff, Youth Players) and amortization of players’ costs. Respectively, these stand at €182M and €90M. And I am certain that signing players like Romelu Lukaku – whilst brilliant on the field – must have hurt the club even further this year. His wages, over €7.5M net (approximately €13M Gross) and the €5M loan fee are numbers that for a club like AS Roma, at this time, have surely not helped. This is most likely the case if we then consider how little success the club has gathered in Italy and significant European competitions (such as qualifying or making a run in the UEFA Champions League) over the past few years.

Now, whilst wages and amortization data on their own do not paint a problematic picture, the fact that the club is only bringing in revenues of €191M (same exact number as the previous year which was deeply affected by COVID-19) undoubtedly does. In my opinion, Romes’s oldest club has failed to modernize and keep up with the pace of other Italian and European clubs over the years. This can be proved in a variety of ways. Above all, the fact that the club only brought in €8M from sponsorships is quite frankly embarrassing. A historic name like AS Roma, home to a myriad of football’s greatest talents over time, should be bringing in larger sums than a mere €8M in sponsorship revenue. For comparison, that same year, Inter Milan brought in almost €50M from sponsors. To fans, potential investors, and the owners, this is the first of many points of evidence as to why AS Roma should arguably not be considered in the ‘big club’ conversation in Italy. Whilst it is wise to give the club the benefit of the doubt for such scarce income from sponsorships due to the pandemic’s impacts, it is important to consider that AS Roma’s history of main sponsors has been very fragile. As a fan of the league, I quite frankly recall more sponsor-less AS Roma jerseys than jerseys with a main sponsor — and that, to me, tells a clear tale.

On top of this, whilst the club has notable income from TV revenues at €80M, it is also lacking in terms of game revenue. Bringing in €14M from UEFA participation and performance bonuses and €25M from ticket sales is simply not enough if you consider the magnitude of the club’s expenses and the way the club tend to position themselves in ‘big club’ conversations. What’s the issue here? Definitely not the AS Roma fans, loyal and warm as always with an average attendance of over 60 000 fans per game. The issue is, perhaps, an outdated and city-owned stadium like the Stadio Olimpico of Rome. Like with most other Serie A clubs, AS Roma has an urgent need to remodel their strategy in terms of ticket sales and stadium. In between them and a modernized stadium (which not only would bring its assets’ and the club’s value up) stands Italian bureaucracy — which has been the theme in most stadium development projects all around Italy. As mentioned in Inter’s Financial Analysis and AC Milan’s Sports Business Article, the model to follow is Tottenham Hotspur and their brand new Tottenham Hotspur Stadium. Benefits like full ownership and the ability to open up other streams of revenue from events like concerts would be invaluable to the Capitolino club. This is especially the case if we consider AS Roma’s Net Assets, which read a drastic -€340M. In other words, the club doesn’t own too much that might lure in new investors, and its liabilities exceed the value of its assets.

But Umberto, why would we care about the costs and losses? And what about the debts? It seems like every club in Italy is running on debt, is that a problem?

Right, you raise a fair point. As mentioned, Roma operates at a continuous loss year after year, with the 2021-2022 fiscal year producing a net loss of €200M. On top of this, the club has €470M of debt, which paints an unhealthy financial picture to say the least. Why is this the case? I hear you ask. Even though seeing “negative” numbers is never the most encouraging thing to see when talking about finances, there are more reasons as to why Roma’s debt and continuous losses should scare the fans.

First of all, cash flow is extremely reduced as a result of debt repayments. Cash flow is something rather fragile for the club, too. Dan Friedkin, owner of the club, has poured in over €500M in as part of financing activities to cover operating and investing activities. This is also known as equity share capital (or equity financing), and sees the club issue new shares in exchange for the money. Specifically, over the 2021-2022 year, AS Roma burned through €100M in operating activities (running the club on a daily basis) and €76M in investing activities (capital expenditures, future projects), and Dan Friedkin covered that with €180M of capital. In terms of the big picture, this means that the club keeps operating at a loss and has to keep “putting more money” into the club to ensure that it has a positive cashflow, a requirement for a Serie A club to start a season. Further, losses often lead to taking on more debt as a result of covering shortfalls in money. We could also argue that a vicious cycle of debt and losses, eventually, leads to bankruptcy or failure. This is because if the cycle worsens there’ll come a point where cash cannot be injected into the business at such high rates, and the debts (which also have interest) will not be covered or refinanced.

Now, if we look at the bigger picture with all of the aforementioned in mind, we can draw a few conclusions. Above all, the club is close to being worthless. Negative net assets, debts, continuous losses, and most importantly, the club doesn’t win competitions that bring in money. Plus, the fact that the club was delisted from the Stock Exchange after twenty-two years doesn’t exactly overwhelm me with confidence. And whilst we may never know the real reason, we could speculate that the board of executives at the club deemed its financial situation – which has to be public for a business listed on a stock exchange – to be too dire and potentially sway investors off of the Appian road. Truthfully, who would want to buy or save a club in these conditions? To me, when Dan Friedkin gets tired of pouring cash (or simply runs out of it) into the club, there’ll be low chances of him selling the club for a reasonable amount. For this exact reason, I can’t help but believe that Serie A club owners must have such strong passions towards these teams — Calcio will never bring money in for these wealthy, savvy businessmen like Dan Friedkin.

Nevertheless, like with every club, there is a way out. In terms of strengths, the club still holds immense historical value and a true group of aficionados, tifosi. A new stadium with new sponsorships to increase revenues, cutting costs from operating activities, wages, and amortization, and a new player trading strategy would be huge steps for the Capitolino club. Enough of the old, high-wage players, and in with new, young, scouted players. Lower costs and greater chances to set up capital gains. To me, AS Roma should also look inside — which is exactly what manager Josè Mourinho has started to do over the past year. More trust to players from the Primavera (U19 team), which has been known for producing various talents over the years like Lorenzo Pellegrini and Riccardo Calafiori, will eventually produce players that can be sold and bring in incremental revenues. But above all, the club and its fans must accept the fact that there’ll have to be a “reconstruction phase” like all major clubs have had and move, together, towards a common goal: success for AS Roma.

Works Cited:

“Bilancio Consolidato AS Roma Stagione 2021-2022”, AS Roma, 2022